Selling Your House? Your Asking Price Matters More Now Than Ever

There’s no doubt about the fact that the housing market is slowing from the frenzy we saw over the past two years. But what does that mean for you if you’re thinking of selling your house?

While home prices are still appreciating in most markets and experts say that will continue, they’re climbing at a slower pace because rising mortgage rates are creating less buyer demand. Because of this, there are more homes on the market. And in a shift like this one, the way you price your home matters more than ever.

Why Today’s Housing Market Is Different

During the pandemic, sellers could price their homes higher because demand was so high, and supply was so low. This year, things are shifting, and that means your approach to pricing your house needs to shift too.

Because we’re seeing less buyer demand, sellers have to recognize this is a different market than it was during the pandemic. Here’s what’s at stake if you don’t.

Why Pricing Your House at Market Value Matters

The price you set for your house sends a message to potential buyers. If you price it too high, you run the risk of deterring buyers.

When that happens, you may have to lower the price to try to reignite interest in your house when it sits on the market for a while. But be aware that a price drop can be seen as a red flag for some buyers who will wonder what that means about the home or if in fact it’s still overpriced. Some sellers aren’t adjusting their expectations to today’s market, and realtor.com explains the impact that’s having:

“. . . the share of listings with a price cut was nearly double its year ago level even as it remains well below pre-pandemic levels.”

To avoid the headache of having to lower your price, you’ll want to price it right from the onset. A real estate advisor knows how to determine that perfect asking price. To find the right price, they balance the value of homes in your neighborhood, current market trends and buyer demand, the condition of your house, and more.

Not to mention, pricing your house fairly based on market conditions increases the chance you’ll have more buyers who are interested in purchasing it. This helps lead to stronger offers and a greater likelihood it’ll sell quickly.

Why You Still Have an Opportunity When You Sell Today

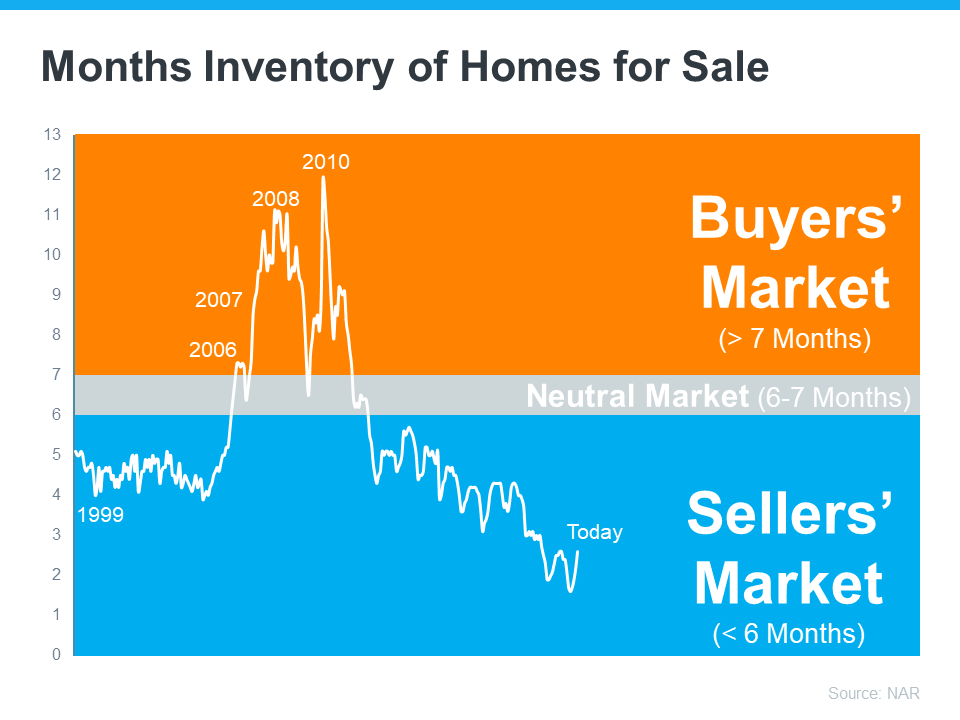

Rest assured, it’s still a sellers’ market, and you’ll still get great benefits if you plan accordingly and work with an agent to set your price at the current market value. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Homes priced right are selling very quickly, but homes priced too high are deterring prospective buyers.”

Mike Simonsen, the Founder and CEO of Altos Research, also notes:

“We can see that demand is still there for the homes that are priced properly.”

Bottom Line

Home priced right are selling quickly in today’s real estate market. Let’s connect to make sure you price your house based on current market conditions so you can maximize your sales potential and minimize your hassle in a shifting market.

![Housing Market Forecast for the Rest of 2022 [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2022/08/04103828/20220805-KCM-Share-549x300.png)

![Housing Market Forecast for the Rest of 2022 [INFOGRAPHIC] | Simplifying The Market](https://files.simplifyingthemarket.com/wp-content/uploads/2022/08/04103823/20220805-MEM.png)